Riskfolio-Lib Tutorial:¶

__[Financionerioncios](https://financioneroncios.wordpress.com)__

__[Orenji](https://www.linkedin.com/company/orenj-i)__

__[Riskfolio-Lib](https://riskfolio-lib.readthedocs.io/en/latest/)__

__[Dany Cajas](https://www.linkedin.com/in/dany-cajas/)__

Tutorial 13: Riskfolio-Lib and Xlwings¶

1. Downloading the data:¶

In [1]:

import numpy as np

import pandas as pd

import yfinance as yf

import warnings

warnings.filterwarnings("ignore")

pd.options.display.float_format = '{:.4%}'.format

# Date range

start = '2016-01-01'

end = '2019-12-30'

# Tickers of assets

assets = ['JCI', 'TGT', 'CMCSA', 'CPB', 'MO', 'APA', 'MMC', 'JPM',

'ZION', 'PSA', 'BAX', 'BMY', 'LUV', 'PCAR', 'TXT', 'TMO',

'DE', 'MSFT', 'HPQ', 'SEE', 'VZ', 'CNP', 'NI', 'T', 'BA']

assets.sort()

# Downloading data

data = yf.download(assets, start = start, end = end)

data = data.loc[:,('Adj Close', slice(None))]

data.columns = assets

[*********************100%***********************] 25 of 25 completed

In [2]:

# Calculating returns

Y = data[assets].pct_change().dropna()

display(Y.head())

| APA | BA | BAX | BMY | CMCSA | CNP | CPB | DE | HPQ | JCI | ... | NI | PCAR | PSA | SEE | T | TGT | TMO | TXT | VZ | ZION | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2016-01-05 | -2.0257% | 0.4057% | 0.4035% | 1.9693% | 0.0180% | 0.9305% | 0.3678% | 0.5783% | 0.9483% | -1.1954% | ... | 1.5881% | 0.0212% | 2.8236% | 0.9758% | 0.6987% | 1.7539% | -0.1730% | 0.2410% | 1.3734% | -1.0857% |

| 2016-01-06 | -11.4863% | -1.5879% | 0.2412% | -1.7557% | -0.7727% | -1.2473% | -0.1736% | -1.1239% | -3.5867% | -0.9551% | ... | 0.5547% | 0.0212% | 0.1592% | -1.5646% | -0.1466% | -1.0155% | -0.7653% | -3.0048% | -0.9034% | -2.9145% |

| 2016-01-07 | -5.1389% | -4.1922% | -1.6573% | -2.7699% | -1.1047% | -1.9769% | -1.2207% | -0.8855% | -4.6059% | -2.5394% | ... | -2.2066% | -3.0309% | -1.0410% | -3.1557% | -1.6148% | -0.2700% | -2.2845% | -2.0570% | -0.5492% | -3.0019% |

| 2016-01-08 | 0.2737% | -2.2705% | -1.6037% | -2.5425% | 0.1099% | -0.2241% | 0.5707% | -1.6402% | -1.7641% | -0.1649% | ... | -0.1538% | -1.1366% | -0.7308% | -0.1448% | 0.0895% | -3.3839% | -0.1117% | -1.1386% | -0.9719% | -1.1254% |

| 2016-01-11 | -4.3384% | 0.1693% | -1.6851% | -1.0215% | 0.0915% | -1.1791% | 0.5674% | 0.5287% | 0.6616% | 0.0330% | ... | 1.6435% | 0.0000% | 0.9869% | -0.1450% | 1.2224% | 1.4570% | 0.5367% | -0.4607% | 0.5800% | -1.9918% |

5 rows × 25 columns

In [3]:

import riskfolio as rp

# Building the portfolio object

port = rp.Portfolio(returns=Y)

# Calculating optimal portfolio

# Select method and estimate input parameters:

method_mu='hist' # Method to estimate expected returns based on historical data.

method_cov='hist' # Method to estimate covariance matrix based on historical data.

port.assets_stats(method_mu=method_mu, method_cov=method_cov)

# Estimate optimal portfolio:

model='Classic' # Could be Classic (historical), BL (Black Litterman) or FM (Factor Model)

rm = 'MV' # Risk measure used, this time will be variance

obj = 'Sharpe' # Objective function, could be MinRisk, MaxRet, Utility or Sharpe

hist = True # Use historical scenarios for risk measures that depend on scenarios

rf = 0 # Risk free rate

l = 0 # Risk aversion factor, only useful when obj is 'Utility'

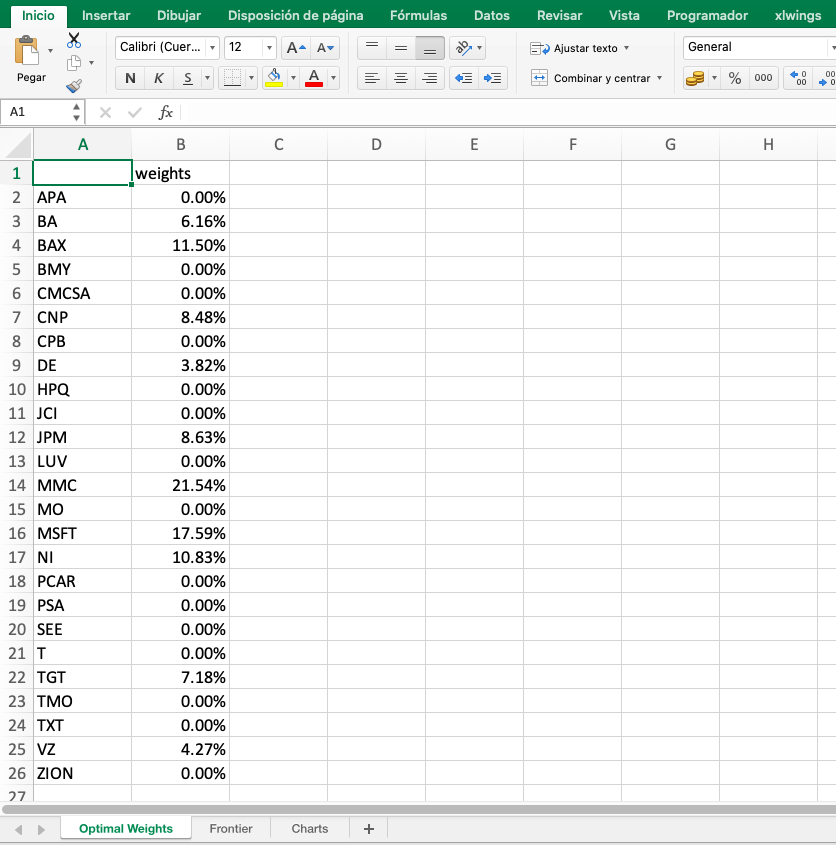

w = port.optimization(model=model, rm=rm, obj=obj, rf=rf, l=l, hist=hist)

display(w.T)

| APA | BA | BAX | BMY | CMCSA | CNP | CPB | DE | HPQ | JCI | ... | NI | PCAR | PSA | SEE | T | TGT | TMO | TXT | VZ | ZION | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| weights | 0.0000% | 6.1590% | 11.5019% | 0.0000% | 0.0000% | 8.4807% | 0.0000% | 3.8193% | 0.0000% | 0.0000% | ... | 10.8262% | 0.0000% | 0.0000% | 0.0000% | 0.0000% | 7.1805% | 0.0000% | 0.0000% | 4.2738% | 0.0000% |

1 rows × 25 columns

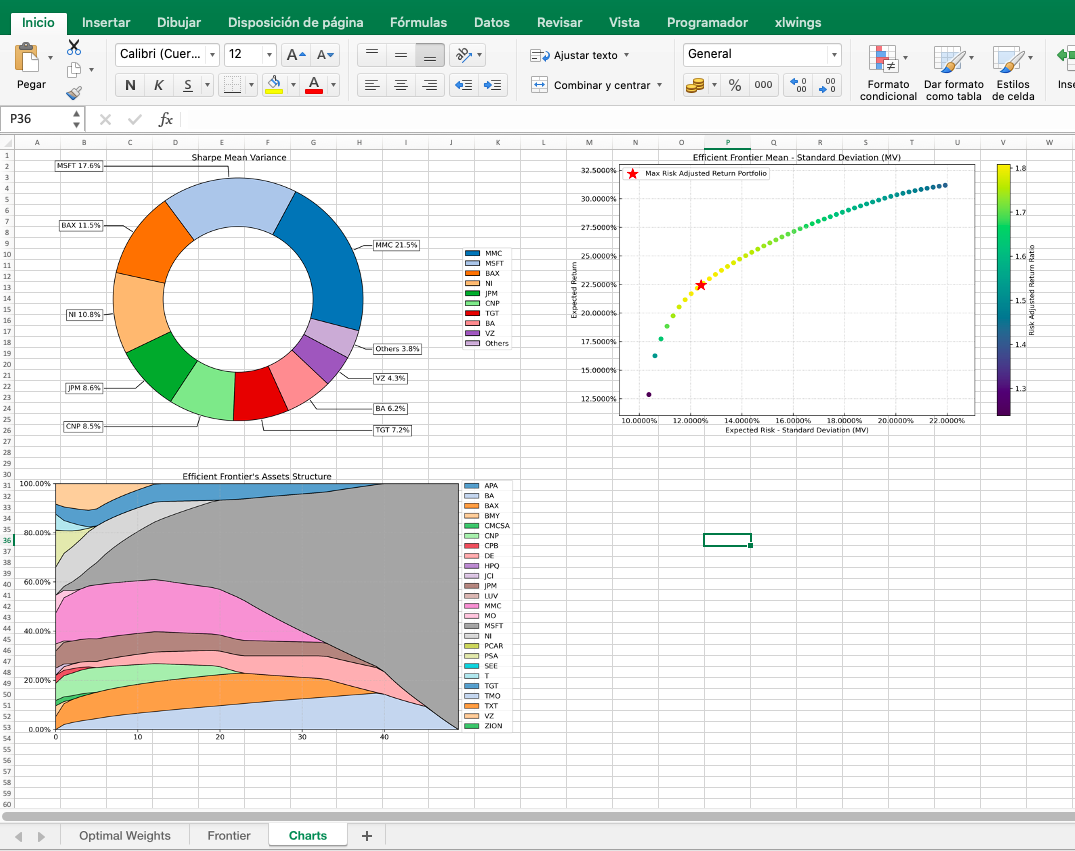

2.2 Plotting portfolio composition¶

In [4]:

import matplotlib.pyplot as plt

# Plotting the composition of the portfolio

fig_1, ax_1 = plt.subplots(figsize=(10,6))

ax_1 = rp.plot_pie(w=w, title='Sharpe Mean Variance', others=0.05, nrow=25, cmap = "tab20",

height=6, width=10, ax=ax_1)

2.3 Calculate efficient frontier¶

In [5]:

points = 50 # Number of points of the frontier

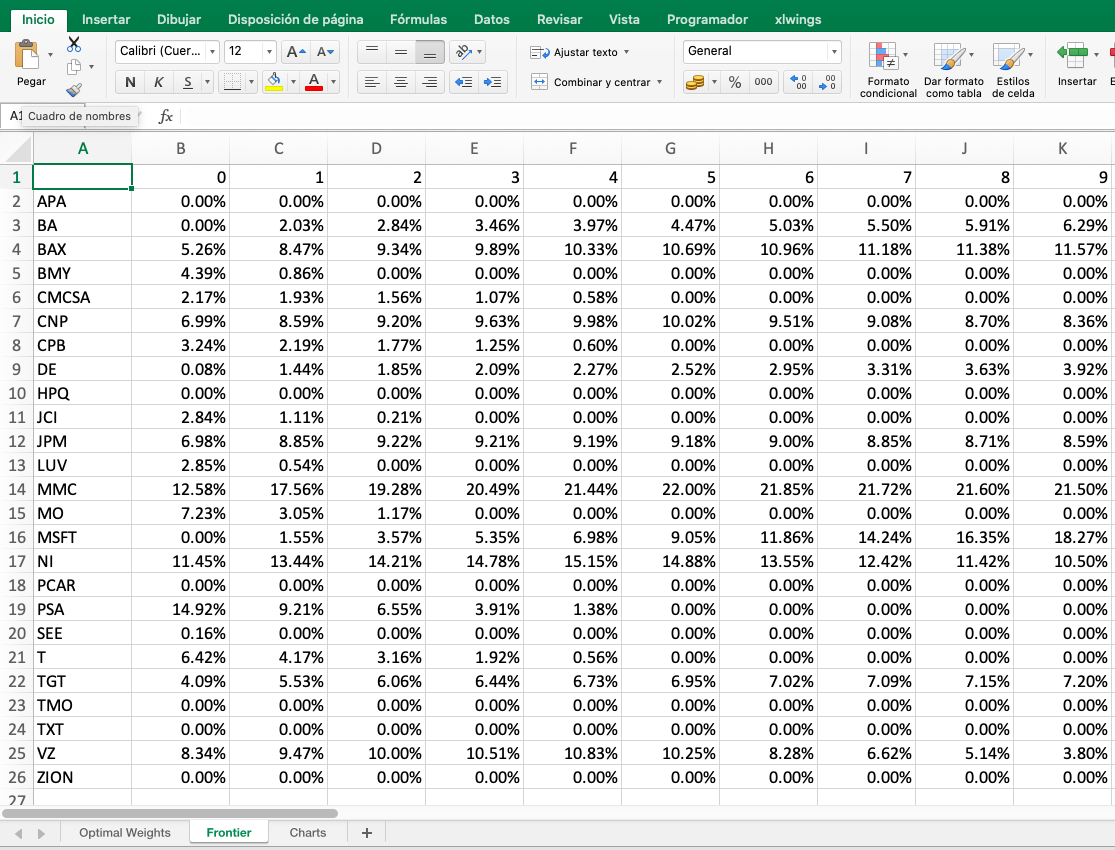

frontier = port.efficient_frontier(model=model, rm=rm, points=points, rf=rf, hist=hist)

display(frontier.T.head())

| APA | BA | BAX | BMY | CMCSA | CNP | CPB | DE | HPQ | JCI | ... | NI | PCAR | PSA | SEE | T | TGT | TMO | TXT | VZ | ZION | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.0000% | 0.0000% | 5.2634% | 4.3887% | 2.1705% | 6.9871% | 3.2390% | 0.0790% | 0.0000% | 2.8377% | ... | 11.4508% | 0.0000% | 14.9184% | 0.1628% | 6.4196% | 4.0904% | 0.0000% | 0.0000% | 8.3446% | 0.0001% |

| 1 | 0.0000% | 2.0325% | 8.4718% | 0.8579% | 1.9327% | 8.5940% | 2.1945% | 1.4376% | 0.0000% | 1.1060% | ... | 13.4410% | 0.0000% | 9.2132% | 0.0000% | 4.1682% | 5.5285% | 0.0000% | 0.0000% | 9.4731% | 0.0000% |

| 2 | 0.0000% | 2.8407% | 9.3407% | 0.0000% | 1.5588% | 9.1990% | 1.7699% | 1.8516% | 0.0000% | 0.2108% | ... | 14.2140% | 0.0000% | 6.5518% | 0.0000% | 3.1594% | 6.0608% | 0.0000% | 0.0000% | 9.9971% | 0.0000% |

| 3 | 0.0000% | 3.4597% | 9.8935% | 0.0000% | 1.0711% | 9.6311% | 1.2504% | 2.0914% | 0.0000% | 0.0000% | ... | 14.7829% | 0.0000% | 3.9064% | 0.0000% | 1.9201% | 6.4433% | 0.0000% | 0.0000% | 10.5067% | 0.0000% |

| 4 | 0.0000% | 3.9674% | 10.3314% | 0.0000% | 0.5839% | 9.9784% | 0.6012% | 2.2744% | 0.0000% | 0.0000% | ... | 15.1468% | 0.0000% | 1.3826% | 0.0000% | 0.5558% | 6.7335% | 0.0000% | 0.0000% | 10.8300% | 0.0000% |

5 rows × 25 columns

In [6]:

# Plotting the efficient frontier

label = 'Max Risk Adjusted Return Portfolio' # Title of point

mu = port.mu # Expected returns

cov = port.cov # Covariance matrix

returns = port.returns # Returns of the assets

fig_2, ax_2 = plt.subplots(figsize=(10,6))

rp.plot_frontier(w_frontier=frontier, mu=mu, cov=cov, returns=returns, rm=rm,

rf=rf, alpha=0.01, cmap='viridis', w=w, label=label,

marker='*', s=16, c='r', height=6, width=10, ax=ax_2)

Out[6]:

<AxesSubplot:title={'center':'Efficient Frontier Mean - Standard Deviation (MV)'}, xlabel='Expected Risk - Standard Deviation (MV)', ylabel='Expected Return'>

In [7]:

# Plotting efficient frontier composition

fig_3, ax_3 = plt.subplots(figsize=(10,6))

rp.plot_frontier_area(w_frontier=frontier, cmap="tab20", height=6, width=10, ax=ax_3)

Out[7]:

<AxesSubplot:title={'center':"Efficient Frontier's Assets Structure"}>

In [8]:

import xlwings as xw

# Creating an empty Excel Workbook

wb = xw.Book()

sheet1 = wb.sheets[0]

sheet1.name = 'Charts'

sheet2 = wb.sheets.add('Frontier')

sheet3 = wb.sheets.add('Optimal Weights')

3.2 Adding Pictures to Sheet 1¶

In [9]:

sheet1.pictures.add(fig_1, name = "Weights",

update = True,

top = sheet1.range("A1").top,

left = sheet1.range("A1").left)

sheet1.pictures.add(fig_2, name = "Frontier",

update = True,

top = sheet1.range("M1").top,

left = sheet1.range("M1").left)

sheet1.pictures.add(fig_3, name = "Composition",

update = True,

top = sheet1.range("A30").top,

left = sheet1.range("A30").left)

Out[9]:

<Picture 'Composition' in <Sheet [Libro2]Charts>>

3.2 Adding Data to Sheet 2 and Sheet 3¶

In [10]:

# Writing the weights of the frontier in the Excel Workbook

sheet2.range('A1').value = frontier.applymap('{:.6%}'.format)

# Writing the optimal weights in the Excel Workbook

sheet3.range('A1').value = w.applymap('{:.6%}'.format)